OK what's this dumpage all about? The excuses proffered so far:

*Sub-Prime Contagion

*Removal of uptick rule for shorts

*Yen carry trade unwind

*Funds cashing out to build a war chest.

Let's look at these one at a time.

*Sub-Prime Contagion - Well Duh!!! All the Wally's who said it was all contained should be tied up to posts and their tongues cut out. Of course it was going to take out the rest of the economy... 'nuf said?

*Removal of uptick rule for shorts - Absolute BS! Institutions have been able to do it (shortsell without an uptick) via derivative proxies forever. It's only the small fry like us that can now do this now... and we have always been able to do it with futures... erroneous at best.

*Yen carry trade unwind - Empirically, this is not only back on the agenda, but looks to serious. While the Dollar has been in a strong retrace against Euro, Pound, AUD etc, it is getting absolutely poleaxed by the Yen. The carry trade is unwinding and unwinding fast.

*Funds cashing out to build a war chest. - According to at least one money manager, the evidence is in the oilers being crunched in the face of rising crude. Conclusion - the funds want CASH.

... and look at treasuries. There is mountains of cash going there in the face of a crising interest rate environment as safe haven. Expect some volatility there!

IMO, This is the beginning of the credit bubble apocalypse. The $417 is finally hitting the fan. This is not to say we go straight down from here, but we should be aware of that possibility... and at least expect massive VOLATILITY.

Cheers... be careful folks.

__________________

27 July 2007

17 July 2007

CDOs and Toxic Debt

From Australian TV ABC Lateline program. Economics reporter Stephen Long talks about the US sub-prime mortgage market , Collateralized Debt Obligations (CDOs) and the collapse of two Bear Stears hedge funds, and the potential for this to set off a global credit crash.

Quote: "The day of reckoning is nigh"

Quote: "The day of reckoning is nigh"

10 July 2007

Bond Apocalypse Averted - For Now

Well my picture perfect 10yr t-note trade with all its bearish connotations has been scuppered over the last to sessions by none other than, err... the bears.

NEW YORK, July 10 (Reuters) - U.S. Treasuries rallied on Tuesday as investors poured out of stocks and speculative bonds for the relative safety of U.S. government securities.

The drive to Treasuries was fed by mounting concern over subprime mortgage debt and the deteriorating housing market that could also hurt U.S stocks, analysts and trader said.

Earnings warnings from retailers and home builders and also credit rating agency Standard & Poor's statement that it may cut ratings of some subprime loans and is reviewing its ratings of collateralized debt obligations were all factors hurting equities and nongovernment bonds.

"It has to do with the S&P headline on subprime. Credit spreads are blowing out. The fear is that they will force selling by those investors who can't hold on to these low investment-grade bonds," said Carl Lantz, U.S. interest rate strategist at Credit Suisse in New York. >>MORE<<

Interestingly, the technically sloppy short setup on the EuroBund has turned up a better looking long trade from a nice double bottom. A long case good certainly be made for the US contract as well, perhaps more so... but I was short. :-P

What has actually happened is that my bond apocalypse has turned into a USD apocalypse, with basically the same reasons quoted; sub-prime/housing slowdown blah blah. This has caused quite some technical damage to the USD index with new lows printed.

For the bulls it really is head in the sand time (if they want to stay bulls). In my humble and ill-educated opinion, the anglo economies are fucked, and are living on borrowed time (and whacking great piles of borrowed money). It will just take a bit of time for muppets to realize this fact.

The precise route by which this financial apocalypse plays out though, is anyones guess.

07 July 2007

Weekend update on Treasuries

Just a quick chart update on my latest obsession in the treasury markets. The short trade setup triggered nicely and has continued in the desired direction. The 10 year T-Notes that I trade are now roughly at the first point of possible (and tenuous IMO) support and not really showing any signs of stopping at this stage.

The other contract I follow is the EUREX Euro Bund. Although the setup wasn't as technically crisp as the t-notes, it was still a valid short setup that triggered a bit earlier while the yanks were messing around and tyeing firecrackers to their neighbor's cat's tail and other pyrotechnical frivolities.

The bund is actually now testing contract lows, a point interest rate obsessed equity investors deem to have missed at this point... or are ignoring.

... or maybe they are expecting support.

The other contract I follow is the EUREX Euro Bund. Although the setup wasn't as technically crisp as the t-notes, it was still a valid short setup that triggered a bit earlier while the yanks were messing around and tyeing firecrackers to their neighbor's cat's tail and other pyrotechnical frivolities.

The bund is actually now testing contract lows, a point interest rate obsessed equity investors deem to have missed at this point... or are ignoring.

... or maybe they are expecting support.

05 July 2007

Next Leg Down For Treasuries?

Earlier in the week I highlighted a setup in 10 year t-notes. Aggressive traders may have taken a short trade straight of that setup, others may wait for a confirmation of price breaking below the trendline. Those waiting got their trigger today.

However there was clue that this would definitely break down in the price action of the Eurobund, which put in a nasty down day on tuesday and has continues down since.

Now things get very interesting, and not just for bonds. Equities are not likely to react well to lower bond prices and the US indices are off a few points as a result.

Technically, there are some obvious points of possible support, but below Junes low folks will likely start shitting themselves. As several commentators have pointed out recently, the market is starting to do what the Fed refuses to do... and should do.

Elswhere, the Brit have jacked rates up another quarter (but should have gone .5), and the Eurozone is announcing later today.

However there was clue that this would definitely break down in the price action of the Eurobund, which put in a nasty down day on tuesday and has continues down since.

Now things get very interesting, and not just for bonds. Equities are not likely to react well to lower bond prices and the US indices are off a few points as a result.

Technically, there are some obvious points of possible support, but below Junes low folks will likely start shitting themselves. As several commentators have pointed out recently, the market is starting to do what the Fed refuses to do... and should do.

Elswhere, the Brit have jacked rates up another quarter (but should have gone .5), and the Eurozone is announcing later today.

04 July 2007

Peter Schiff verses Everyone

Peter Schiff on Kudlow and Company

And the winner is... well that depends on your cognitive biases.

Always entertaining.

And the winner is... well that depends on your cognitive biases.

Always entertaining.

03 July 2007

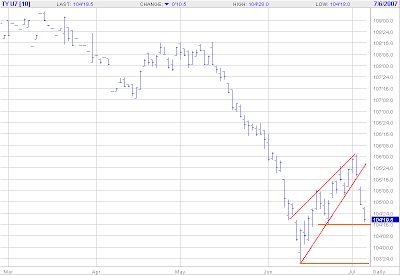

10 Yr T-Notes Setting Up

In the early part of June, US treasuries were responsible for some extreme consternation in the equities market due to to their rabid decent into the nether regions of recent price history. (Inverse relationship to interest rates. Bonds down = interest rates up, for those who don't know). From the highs in June at ~108½ on the September 1o year T-note contract, prices plunged all the way to under 104 in a month.

This really caught the attention of an interest rate obsessed equities market. Although the chart doesn't really show it, it put the wind up those who are awake to the risks.

The recent retracement of that move has meant that folks have lapsed back into their easy credit induced trance. However at this point there is an interesting technical setup shown here on the above mentioned contract.

The retracement has taken us to 50% of that move, which followers of Fibonacci and Gann swear is significant. For me, enough follow this theory to make me sit up and take notice, particularly a setup as clean as this.

Aggressive traders might already have gone short already; others may be looking for some confirmation in the price dropping through the support line. I'll be interested in what else happens if the bond dumpage continues.

It could get very interesting.

This really caught the attention of an interest rate obsessed equities market. Although the chart doesn't really show it, it put the wind up those who are awake to the risks.

The recent retracement of that move has meant that folks have lapsed back into their easy credit induced trance. However at this point there is an interesting technical setup shown here on the above mentioned contract.

The retracement has taken us to 50% of that move, which followers of Fibonacci and Gann swear is significant. For me, enough follow this theory to make me sit up and take notice, particularly a setup as clean as this.

Aggressive traders might already have gone short already; others may be looking for some confirmation in the price dropping through the support line. I'll be interested in what else happens if the bond dumpage continues.

It could get very interesting.

02 July 2007

A Look At Metals Volatilities

Implied volatilities in the metals I trade (gold, silver & copper) are at the moment, at somewhat of a low. If we go by the traditional option dogma of buying options when vols are low, then on face value, metals options are a buy.

But are they. In my experience, it is not as straight forward as that. Well if you have a clear directional view of an imminent move, then sure, buy a call or a put, or the directional spread of your choice.

The first thing about low volatilities, is that they can stay low for a LONG time, or even go lower. This is generally not a good thing if you are long options. An option trade is also a volatility bet to a greater or lesser degree, depending on the strategy. When we buy options, we are long "vega" which means we preferably want volatility to increase, or at least we want the underlying to start trending. If not, we get chopped to pieces by theta (time decay). If volatility decreases, we lose again.

Lets have a look at the volatility picture of Gold (Copper is quite similar):

IVs are basically a third of what they were a year ago and as yo can see they have been even lower. If the unceasingly bullish Gold Bugs are correct, gold will skyrocket as this credit bubble unravels. Not only will gold fly, but gold IVs will also go berserk. Equally though, I have read credible articles that say go will go the same way as housing, into the pits. Who knows?

IVs are basically a third of what they were a year ago and as yo can see they have been even lower. If the unceasingly bullish Gold Bugs are correct, gold will skyrocket as this credit bubble unravels. Not only will gold fly, but gold IVs will also go berserk. Equally though, I have read credible articles that say go will go the same way as housing, into the pits. Who knows?

The big question is if gold makes a big move, when will it be? Well I have no freakin' idea, but let me show you Silver IVs over th last 2 years:

A similar picture to gold, but with an interesting lift in IV on the back of last weeks dumpage.

A similar picture to gold, but with an interesting lift in IV on the back of last weeks dumpage.

Whether this means anything or represents an opportunity, I am pleading the 5th, but I say it's interesting enough for a post on my blog and something to definitely follow.

Stay tuned.

But are they. In my experience, it is not as straight forward as that. Well if you have a clear directional view of an imminent move, then sure, buy a call or a put, or the directional spread of your choice.

The first thing about low volatilities, is that they can stay low for a LONG time, or even go lower. This is generally not a good thing if you are long options. An option trade is also a volatility bet to a greater or lesser degree, depending on the strategy. When we buy options, we are long "vega" which means we preferably want volatility to increase, or at least we want the underlying to start trending. If not, we get chopped to pieces by theta (time decay). If volatility decreases, we lose again.

Lets have a look at the volatility picture of Gold (Copper is quite similar):

IVs are basically a third of what they were a year ago and as yo can see they have been even lower. If the unceasingly bullish Gold Bugs are correct, gold will skyrocket as this credit bubble unravels. Not only will gold fly, but gold IVs will also go berserk. Equally though, I have read credible articles that say go will go the same way as housing, into the pits. Who knows?

IVs are basically a third of what they were a year ago and as yo can see they have been even lower. If the unceasingly bullish Gold Bugs are correct, gold will skyrocket as this credit bubble unravels. Not only will gold fly, but gold IVs will also go berserk. Equally though, I have read credible articles that say go will go the same way as housing, into the pits. Who knows?The big question is if gold makes a big move, when will it be? Well I have no freakin' idea, but let me show you Silver IVs over th last 2 years:

A similar picture to gold, but with an interesting lift in IV on the back of last weeks dumpage.

A similar picture to gold, but with an interesting lift in IV on the back of last weeks dumpage.Whether this means anything or represents an opportunity, I am pleading the 5th, but I say it's interesting enough for a post on my blog and something to definitely follow.

Stay tuned.

Subscribe to:

Posts (Atom)